Analysis: Competition hots up as British banks fight to keep earnings rising faster than costs

British banks face a tougher battle for mortgage customers and business borrowers in 2023, as rising costs and deposit rates paid to long-suffering savers threaten to outpace flatlining profit margins, senior industry executives and analysts said.

British banks face a tougher battle for mortgage customers and business borrowers in 2023, as rising costs and deposit rates paid to long-suffering savers threaten to outpace flatlining profit margins, senior industry executives and analysts said.

The 2022 annual results from the country's four biggest lenders in the last week had been expected to show an earnings bonanza as banks increased the rate they charge on loans while leaving deposit rates low.

Instead, despite reporting robust profits, banks' shares have broadly stumbled as they forecast margin pressure, suggesting intensifying competition for customers' deposits and mortage business to come.

"It may be that we've seen the peak of margin," said William Chalmers, finance chief of Britain's biggest domestic bank Lloyds on Wednesday.

"... certainly during the course of 2023, we do expect the margin to come down, reflecting mortgage pricing being more competitive, and likewise us making sure we offer savers the right rates on their products."

After a decade in which rates have sat near zero, giving savers little reason to shift their balances to competitors, the jump in Britain's policy rate to 4% is spurring competition not seen in years.

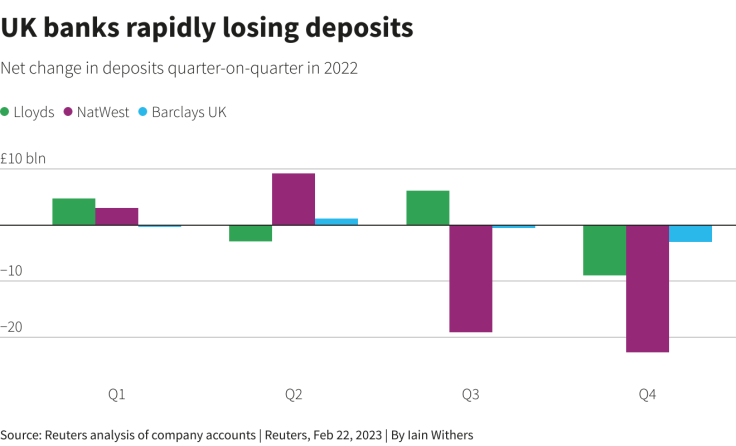

Three of Britain's biggest banks - Lloyds, NatWest and Barclays UK - saw their combined deposits fall by 34.7 billion pounds ($42 billion) in the last three months of 2022 alone, a Reuters analysis of their results shows, partly reflecting a flight by customers in search of higher rates.

GRAPHIC: UK banks rapidly losing deposits

The major banks have faced criticism from politicians for not raising savings rates as swiftly as they have rates on loans.

Lenders are also facing calls from campaigners for a windfall tax on their profits, as seen in the energy sector, after some hiked bonus pools for staff at a time when millions of their customers were struggling with a cost-of-living crisis.

"I think the banks are worried they could face political intervention," said John Cronin, banking analyst at Goodbody, who added that the cautious tone from banks could also reflect concern charges for bad loans could rise faster than expected.

Lenders say they have started to pass on higher rates to savers, adding that profitability is rebounding after years of low margins. But they are still adjusting.

HSBC on Tuesday forecast interest income would be at least $36 billion in 2023, shy of forecasts for $37 billion, in a move that analysts said showed the bank was trying to manage heightened expectations about its performance.

"We haven't seen these levels of rates in a decade, so our assumptions on deposit migration are not based on strong historical data, we need to assess the likely competitive pressure on deposits," HSBC Chief Financial Officer Georges Elhedery told Reuters.

SWITCHING COMEBACK?

Big shifts in Britain's normally cosy banking market are already underway.

Britain's current account switching service, which lets customers swap to a different bank easily, saw 376,107 such moves in the fourth quarter of 2022, the highest level on record.

Pressure to immediately increase the rates banks pay savers has been intensified by the digital offerings from U.S. entrants into the market such as JPMorgan and Goldman Sachs, executives at the top British lenders said.

Both U.S. banks increased their online savings rates within 24 hours of the latest Bank of England interest rate hike, to 3% and 2.8% respectively.

An analysis of data from price comparison website Moneyfacts shows how deposit rates paid to savers have risen in the last year, but also how far they have yet to go to catch up with rising base rates and mortgage costs.

Lloyds' flagship Easy Saver instant access account paid just 0.6% as of Feb. 22, compared with 0.01% as of December 2021, the data showed. NatWest's Flexible Saver instant access account likewise offered 0.65%, up from 0.01% over the same period.

But over the same period both banks have seen an increase of more than 3 percentage points in the rates they charge on standard floating rate mortgages, to 7.49% and 6.74% respectively, Moneyfacts data shows.

HSBC, Barclays, and Lloyds did not immediately respond to Reuters' request for comment.

NatWest referred Reuters to previous management comments that they were offering proactive support to customers who need it. Lloyds and NatWest have said they both offer a range of savings products, including fixed-term products with higher rates.

In contrast to floating rates, which broadly track the Bank of England benchmark, fixed mortgage rates have started to fall as competition intensifies. But the average remains above 4%, Moneyfacts data shows, and the market faces a tough outlook.

Britain faces greater mortgage refinancing risks than the United States or Euro Area because the vast majority of mortgages are fixed for five years or less, analysts at Goldman Sachs said on Wednesday.

Home loan volumes across the sector had plunged to between 1.1-1.2 billion pounds a day, down from 1.5 billion pounds normally, Lloyds said, adding that house prices were likely to drop 7% this year. ($1 = 0.8260 pounds)

Copyright Thomson Reuters. All rights reserved.

- MOST POPULAR IN Finance & Banking