Mervyn King and the Politics of Uncertainty

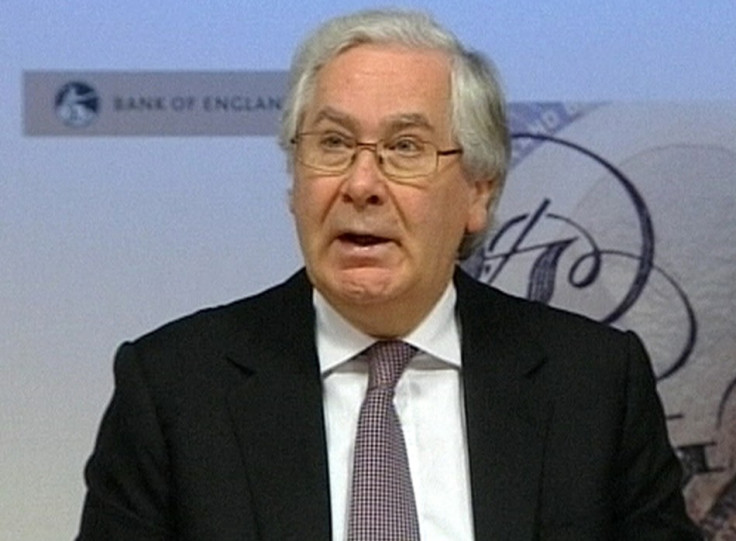

The Bank of England under the direction of its governor Mervyn King today revised down its growth projections for the British economy this year and is now saying that the nation will not reach pre-crisis levels until 2014.

However given that King also claimed that the recovery would be "uncertain" and that there was "no obvious solution" to the greatest inhibitor of recovery - the Euro crisis - there is little reason to believe that we should take the 2014 date any more seriously than failed US presidential contender Newt Gingrich's proposal to build a moonbase by the end of the decade.

Time and time again growth projections have been revised down to the extent that one wonders why anyone bothers making them anymore. As Andrew Neil might put it, economists use decimal points to show they have a sense of humour.

Politically this can hardly be taken as good news for David Cameron and his sidekick George Osborne, both of whom were pinning their 2015 election strategy on the assumption that the economy would clearly be on the mend after five years of Coalition government.

But with the Bank of England saying the economy will not have recovered from the crisis until 2014 at the earliest, Cameron and Osborne might be well advised to assume that in reality the economy will not have reached pre-crises levels until 2015 if at all during their term in office.

The polls are now regularly giving the Labour Party a double-digit lead over the Tories, extraordinary when one considers that the Opposition is now lead by someone who appears to be a sixth-former on work experience and sounds like Sid the Sloth from the Ice Age films.

Is it really possible that in 2015 Britain will turn to Edward Miliband if only to get away from the Tories?

Sadly the only certainty at present is uncertainty. At present Greece is said to be on the verge of leaving the euro and perhaps even the EU and while that may be the end of the story for Greece, it opens up a whole new chapter for Europe and Great Britain.

What will happen to Portugal, Spain and Ireland if Greece defaults and leaves? Will we have to endure the two year process of putting off the inevitable with those nations as we have with Greece, to calamitous effect? What would that do to the Bank of England's current growth projections one wonders?

In addition will the departure of Greece fuel secessionist tendencies in Britain, arguably the EU's most eurosceptic country?

Already the idea of a referendum on EU membership has spread beyond the confines of the growing fringe party UKIP and has been mooted as a possibility by Labour Shadow Chancellor Ed Balls. Given that the Tories got a strong poll bounce last December after David Cameron's so-called veto (whatever happened to that?) heaven knows what will happen to Labour's poll ratings should they come out in favour of a referendum, they might get a 20 point lead.

Such a move, if it ever happens, would almost certainly cause untold chaos on David Cameron's back benches. Who knows, perhaps Jacob Rees-Mogg will stand up in the Commons and declare Miliband to be the "toast of Somerset".

Yet it could also force the Conservatives into also promising a referendum on EU membership, a move which could help attract back enough of its former voters who have drifted off to UKIP in the last few years.

Almost everything in the realms of politics and economics is uncertain at present. Even the fate of the Lib Dems who some might regard as "toast" come the next election.

If it proves to be a tight race, even if the Lib Dems are reduced to a "fit into the back of a cab" party that could still give them enough leverage to form part of yet another coalition. Simon Hughes for Deputy Prime Minister anyone?

© Copyright IBTimes 2025. All rights reserved.

- MOST POPULAR IN Politics