The Death of the Wire Transfer: Why the Digital Entertainment Sector is Shifting to Stablecoins in 2026

From online gaming to global remittances, consumers are abandoning slow, expensive wire transfers in favor of blockchain-based settlement

There is a particular kind of financial friction that has nothing to do with how much money you have. You initiate a payment, the funds are sitting in your account, and the transaction simply fails–declined by your own bank, with no explanation and no recourse. For a growing number of US consumers, this has become routine, and it is quietly reshaping how an entire sector of the economy moves money.

The digital entertainment market is where the shift is most visible. Online gaming and gambling platforms run on high-frequency, time-sensitive, cross-border transactions–exactly the category traditional banking handles worst. US banks increasingly decline payments flagged with gambling-related merchant category codes, a practice rooted in the Unlawful Internet Gambling Enforcement Act of 2006, which pressured payment processors to refuse gambling-related transfers. Debit card acceptance for these merchants has declined steadily since, and bank-initiated blocks have become the norm rather than the exception.

Because domestic banks frequently block gambling merchant codes, the modern player looking for an online casino usa real money experience is now relying almost entirely on offshore platforms that hold balances in native cryptocurrency.

The result is a market that has effectively skipped a generation of payment technology. Where a regulated domestic operator might offer bank transfer, debit card, and e-wallet options, the offshore sector has consolidated around stablecoins, not as an ideological choice, but as the only rail that reliably works. Tether (USDT) on the low-fee Tron network has become the dominant settlement method, precisely because it sidesteps the banking relationships that keep failing.

That makes gambling an unusually clean case study for a much larger financial shift. The same friction — slow settlement, high fees, and intermediary banks that decline transactions with little transparency — shows up across remittances, freelance payments, and digital goods markets. Tether's circulating supply has climbed to roughly $190 billion as of mid-2026, up from around $118 billion at the start of 2025, and a significant share of that growth has come from consumers using the token as a payment rail rather than a speculative asset.

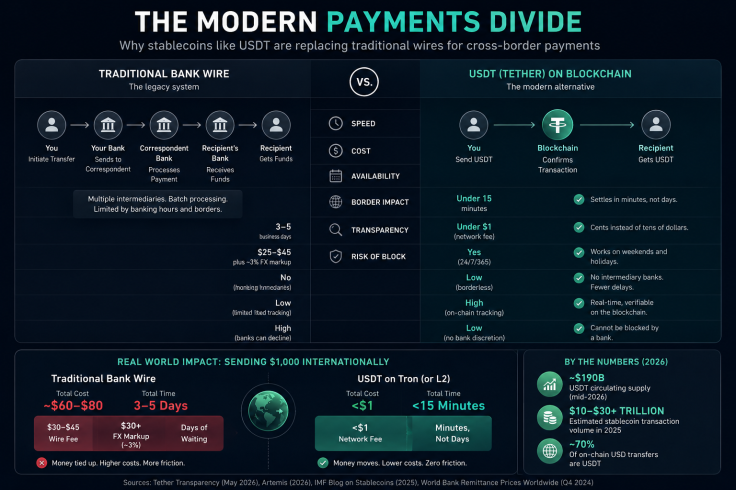

Why are USDT withdrawals faster than fiat?

USDT withdrawals are faster because they bypass the correspondent banking system entirely. A traditional wire passes through multiple intermediary banks, each applying its own batch-processing schedule and compliance checks. A stablecoin transaction settles directly on a blockchain, where confirmation takes minutes regardless of borders, banking hours, or weekends.

The legacy system runs on batch processing, transactions collected, netted between institutions, and settled in cycles that pause overnight, on weekends, and on banking holidays. A wire initiated on a Friday afternoon may not begin processing until Monday. Blockchain settlement has no such schedule; the network runs continuously, and by some estimates roughly seven in ten on-chain dollar transfers now move as USDT rather than any other token.

| Metric | Traditional Bank Wire | USDT (Tether) |

| Average Speed | 3–5 business days | Under 15 minutes |

| Average Fee | $25–$45 plus ~3% FX markup | Under $1 (network fee) |

| Weekend Processing | No | Yes (24/7) |

The fee difference compounds the speed difference. A consumer sending the equivalent of $1,000 internationally by wire can lose $30 in wire fees and another $30 in foreign-exchange markup, roughly 6% of the transaction before it arrives. The same transfer in USDT on a low-fee network costs cents.

Is the shift limited to gambling, or is it broader?

The shift is broader. Gambling is simply where the friction is most acute and the demand for fast settlement is highest, which makes it the leading indicator. The same migration to stablecoins is well underway in remittances, cross-border freelance payments, and any market where consumers move small sums internationally on a frequent basis.

In countries with volatile local currencies — Argentina, Turkey, Nigeria, parts of Southeast Asia — USDT already functions as an informal savings and remittance rail, a use the International Monetary Fund has repeatedly flagged as a dollarisation vector. Stablecoin transaction volume ran into the tens of trillions of dollars over the course of 2025, a figure that now rivals established card networks. The gambling player in the US and the remittance sender in Lagos are, at the payments layer, solving the same problem with the same tool.

What this means for traditional finance

The wire transfer is not disappearing for institutional use, where settlement finality and regulatory clarity still favor the established system. But for consumer cross-border transactions — where speed and cost matter most and transaction sizes are smallest — the economics have decisively shifted.

Banks have responded with faster domestic rails. The US FedNow service and the UK's Faster Payments offer near-instant domestic settlement, and regulatory developments, including the US stablecoin framework and Europe's MiCA regime, have pulled the asset class further into the mainstream. But these new rails are domestic by design. They do little for the cross-border consumer transaction, which remains the stablecoin's home turf.

The death of the wire transfer, then, is not a single event but a slow migration of specific use cases. The high-value, low-frequency institutional wire will persist. The low-value, high-frequency, time-sensitive consumer transaction — the kind the digital entertainment sector runs on by the millions — has already largely moved on. For a financial system built on the assumption that moving money takes time and costs money, that is a generation of consumers concluding the trade-off they inherited was never necessary in the first place.

© Copyright IBTimes 2025. All rights reserved.

- Recommended For You