Janet Yellen, FOMC and UK, EU and Canada Inflation: What to Look Out For

The week to June 20 is marked by the FOMC policy decision and policy meeting minutes from the Bank of England, the Reserve Bank of Australia and the Bank of Japan.

Other G10 central banks in focus are the Swiss National Bank and Norges Bank setting their rates.

The Federal Reserve is not expected to alter rates or its asset purchase programme but the statement and Yellen's press conference will be keenly watched for updated policy signals from the world's largest economy.

The FOMC has been tapering the size of the Fed's monthly bond purchases by $10bn in each of their four previous meetings.

US industrial production probably increased in May for the third time in four months, while housing starts cooled last month, data in the coming week may show.

Recent US data

Data out recently from the US were mixed. ISM manufacturing for April came in at 54.9 from 53.7 in the previous month and consumer price inflation for the month rose to 2.0% y/y and 0.3% m/m from 1.5% and 0.2% respectively.

April non-farm payrolls surprised on the higher side but came in slightly below expectations for May. The unemployment rate, however, came in lower than expected at 6.3% for both the months.

Annualised GDP decreased 1% in Q1, data showed on 29 May, when the market had been expecting a much moderate drop of 0.2%. It had grown 0.1% in the previous quarter.

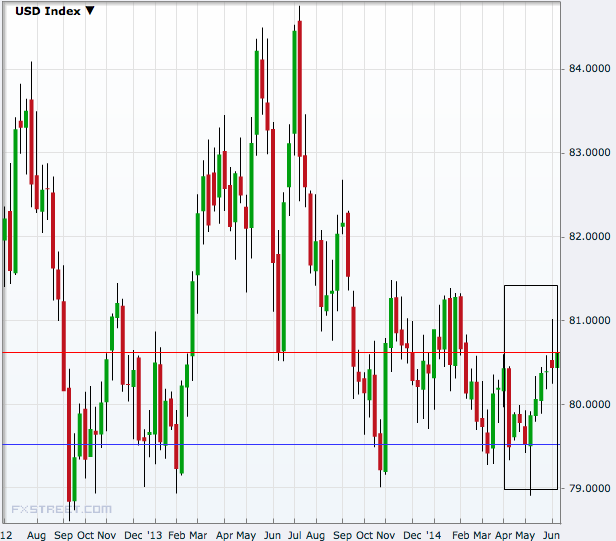

Dollar, risk

The US dollar rallied to four-month highs against the euro and the Swiss franc mainly driven by dovish signals from the European Central Bank while signs of stronger recovery from Japan and the UK weakened the greenback against the yen and the sterling.

Overall the dollar index, the gauge that measure's the greenback's strength against currencies of six largest trading partners, rose to a four-month high, reversing April losses.

Global risk appetite has decreased slightly as rising tensions in Iraq heightened worries that oil supplies will be hit badly but stocks are looking up given the better demand scenario.

Inflation, GDP

Consumer price inflation from the US, the eurozone, the UK and Canada will be watched this week for more policy signals from the respective economies.

US inflation may have stayed at 2% year-on-year while it may have edged higher to 2.1% from 2% in its neighbour Canada. UK inflation may have eased to 1.7% from 1.8% while it may have had a sharper fall to 0.5% from 0.7% in the eurozone

New Zealand GDP data for Q1 will be out on Wednesday; it was up 3.1% y/y and 0.9% m/m in the previous quarter.

Speakers

Fed Chairwoman Janet Yellen's press conference on Wednesday will be the most widely followed remarks this week.

On Tuesday, Reserve Bank of Australia governor Glenn Stevens will speak and on Friday, Bank of Japan's Kuroda will deliver an address.

© Copyright IBTimes 2025. All rights reserved.

- MOST READ